Micro-jurisdictional risk: One of AML’s missing links

High level jurisdiction risk assessments alone are often too broad in scope to include in anti-money laundering policies; Micro-jurisdictional risk analysis could help allay model bias.

- Some aspects of AML policies and procedures are in need of an overhaul, to capture variables important to making accurate analysis

- Low risk jurisdictions have high-risk neighbourhoods and, conversely, not all customers and transactions from high-risk jurisdictions warrant heightened scrutiny

- Financial institutions should go beyond existing AML guidelines and apply a more granular risk-based approach to geography to stay ahead of upcoming best practices

Editor's Note: This article originally appeared on The Asian Banker on May 9, 2017.

High level jurisdiction risk assessments alone are often too broad in scope to include in anti-money laundering policies; Micro-jurisdictional risk analysis could help allay model bias.

- Some aspects of AML policies and procedures are in need of an overhaul, to capture variables important to making accurate analysis

- Low risk jurisdictions have high-risk neighbourhoods and, conversely, not all customers and transactions from high-risk jurisdictions warrant heightened scrutiny

- Financial institutions should go beyond existing AML guidelines and apply a more granular risk-based approach to geography to stay ahead of upcoming best practices

Financial institutions tend to build their anti-money laundering (AML) frameworks based on regulatory guidelines and commonly accepted industry standards. This can include jurisdiction risk, a common input banks use when evaluating customers and their transaction activity to determine degrees of AML risk, or to identify suspicious activity. Jurisdiction risks are based on a number of factors, including links to sanctions, terrorism, narcotics, corruption and other legislative and government deficiencies. The problem with attempting to include jurisdiction risk in AML policies is that it is simply too broad in scope, ranging from entire countries to subcomponents of cities, which lends such analysis to be either overemphasised or underemphasised as a data input.

As an example, there is strong evidence from the US that crime often occurs in High Intensity Drug Trafficking Areas (HIDTA), given the link between violent crime, competing drug distributors, and addicts looking to finance their next fix. HIDTA is an example of a high-risk micro-jurisdiction within the US, and banks may factor this into their lending decisions.

By contrast, foreign micro-jurisdictions have generally not been a component of AML programmes because of the large number of geographic areas which would need to be monitored on an ongoing basis, and the difficulty of defining how a standard of a high-risk micro-jurisdiction could apply across the globe. This leaves a gaping hole in the AML process, which severely limits its potential global impact.

As an example, while Belgium is generally considered to be a country with low credit, compliance, and traveller risk, it has also proven to be a breeding ground for Islamic extremism with a 2016 report by the International Centre for Counter Terrorism in The Hague noting that an estimated 13% of EU foreign fighters in Syria have roots in Belgium - the greatest number per capita of any country in the EU. An issue for Belgium is that information is not consistently shared between law enforcement agencies, making it easy for leads to fall through the cracks. Brussels has six police forces, each reporting to a different mayor. Given that rudimentary intelligence information is such a difficult process, what real chance do national or global law enforcement authorities realistically have to apply AML standards to the transfer of funds between terrorism suspects in Belgium, and between Belgium and destinations in the Middle East?

Other high-risk micro-jurisdictions have been tied to terrorism. Evidence has shown that funding for the 1998 U.S. embassy bombing in Nairobi was through a hawala office in its infamous Eastleigh neighbourhood, an enclave for Somali immigrants. Kenya is generally considered to be high for risk for travellers, with Eastleigh being at elevated risk due to violent crime and terrorist activity. Another example is El Salvador, which became the world’s most violent country in 2016 with its capital, San Salvador, becoming the world’s most homicidal city. San Salvador is clearly another high-risk micro-jurisdiction where law enforcement has itself become a victim of the drugs and gang war, with 49 police officers killed in 2015 alone. High murder rates can imply greater AML risk in specific geographic areas.

Even though a correlation can undoubtedly be made between high-crime neighbourhoods and money laundering, it is worth asking whether financial institutions should be responsible for applying a risk-based approach to these areas, as they would be required to do for other, non-high risk jurisdictions. Clearly there is great need for stripping bias from decision making to enable managers to make better decisions about whether, and how, to apply AML methodologies. Placing greater significance on managing jurisdiction risk would appear to be an important way to create greater awareness among investigators who review customers and their transactions.

However, imagine two publicly traded multinational companies conducting transactions with one another from high-risk jurisdictions. That should automatically be considered high-risk by virtue of geography, because the nature of risk depends on the entities involved, their reputation risk, history, and potential AML exposure. Should there turn out to be a strong correlation between customer risk ratings and jurisdiction risk, it could be a symptom that jurisdiction risk is being overemphasised. The same bias could apply to an institution’s transaction monitoring system, which may generate alerts in proportion to the jurisdiction’s risk level they originate from or terminate in.

Model biases can manifest themselves in any number of areas within an AML programme, including customer due diligence, transaction monitoring and sanctions. Focusing on micro-jurisdictions and other factors linked to transactions can allow for the recalibration of existing models to adapt a more granular risk-based approach. While it may seem like a daunting task to identify high-risk micro-jurisdictions, data is available and can be made useful more easily than many institutions may imagine, with the right approach. It is incumbent upon all financial institutions to go beyond existing AML regulatory guidelines to find the most effective approach to AML. Eventually, the regulations will catch up with emerging best practices.

Keith Furst is founder and financial crimes technology expert of Data Derivatives. Daniel Wagner is managing director of Risk Cooperative and co-author of the book “Global Risk Agility and Decision Making”. The views expressed herein are strictly of the authors.

Why Banks Must Evolve their AML Process to Manage Micro-Jurisdictional Risk

United States sanctions policies have evolved over the years, from country-wide embargos to more nuanced approaches targeting specific entities. According to Jacob J. Lew, Secretary of the Treasury, the sanctions implemented today are more focused on bad actors while trying to limit the negative externalities. Lew described his view on the traditional sanctions model at the Carnegie Endowment for International Peace which is eloquently summarized by this quote:

The Evolution of Sanctions

United States sanctions policies have evolved over the years, from country-wide embargos to more nuanced approaches targeting specific entities. According to Jacob J. Lew, Secretary of the Treasury, the sanctions implemented today are more focused on bad actors while trying to limit the negative externalities. Lew described his view on the traditional sanctions model at the Carnegie Endowment for International Peace which is eloquently summarized by this quote:

Lew went on to describe how the application of sanctions has evolved over the years, and through better financial intelligence, strategy, and design, the new model can home in directly on bad actors:

The Evolution of US Trade Sanctions

The diagram below illustrates the evolution of US Trade Sanctions. Longstanding sanctions would generally indicate a country-wide embargo, as is the case for Cuba and Iran. However, the Cuban and Iranian sanctions policies are currently in transition, as the traditional sanctions model is becoming deemphasized and would now only be used in extreme circumstances such as the case with North Korea. Sanctions imposed on African countries in 2005-2006 as highlighted in the diagram below were targeted sanctions based on human rights violations, concerns of regional stability or entities involved in undermining the democratic process.

Jurisdictional Risk and AML Systems

The evolution of sanctions highlights how US regulators perceive risk. In the case of the African countries outlined above, sanctions were imposed to prevent the flow of money to the groups and individuals participating in local conflicts. The sanctions imposed were designed to prevent or at least slow down human rights violations. The question is, could this same perception of situational and jurisdictional risk be applied to anti-money laundering (AML) systems?

The Traditional AML Model

Cross-border transfers could be monitored based on a number of factors, but generally models are comprised of three main elements:

- Frequency: The number of transfers which occurred within a specific time period. Example: 3 transfers over a rolling 7 day time period.

- Amount: The value of each transfer. Example: A minimum threshold of X dollars could be configured in the monitoring system. Other elements would include round dollar amounts and amounts just below minimum reporting requirements.

- Jurisdictional risk: The risk level or score associated with each country. Example: Transfers flowing through high-risk jurisdictions would generally receive greater scrutiny than similar transactions which only flowed through low-risk jurisdictions based on the financial institution’s country risk ranking.

Financial Crimes Enforcement Network (FinCEN) Regulatory Guidance

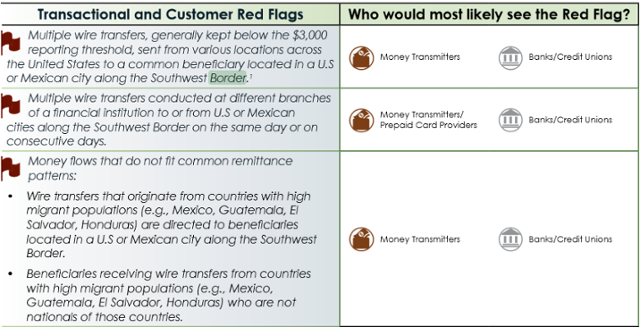

On September 11, 2014 Financial Crimes Enforcement Network (FinCEN) released an advisory guide called “Guidance on Recognizing Activity that May be Associated with Human Smuggling and Human Trafficking – Financial Red Flags” which was intended to help financial institutions identify human trafficking red flags. The interesting part is that FinCEN specifically identified both US and Mexican cities on the Southwest border as areas which require additional scrutiny as described in the transactional and customer red flags listed below:

Source: https://www.fincen.gov/statutes_regs/guidance/pdf/FIN-2014-A008.pdf

Micro-Jurisdictions: The Southwest Border

The image of the Southwest border below illustrates that there are multiple cities in the United States and Mexico that would fall within FinCEN’s advisory.

Micro-Jurisdictions: The Tri-Border Area (TBA)

The Tri-Border area is the region where the borders of Brazil, Argentina, and Paraguay meet, which has been known as a criminal haven for organized crime groups, terror groups and drug traffickers. In a report titled “TERRORIST AND ORGANIZED CRIME GROUPS IN THE TRI-BORDER AREA (TBA) OF SOUTH AMERICA” the author describes various conditions in the Tri-Border Area (TBA) that are very favorable to organized crime and terror groups in the below quote:

The three cities which are highlighted in the report are Ciudad de Este, Foz do Iguaçu and Puerto Iguazú because of their proximity to all three countries’ borders.

Challenges of natural language processing (NLP)

Traditional AML systems usually have functionality to support a list of country codes which can be segmented into categories such as low, medium, high, and very high risk. As a result, transactions which flow through higher risk jurisdictions should, in theory, receive greater scrutiny than lower risk transactions. Financial institutions usually store country codes in various systems based on the International Organization for Standardization (ISO) standard (ISO 3166-1) which can be represented in three formats:

- ISO 3166-1 alpha-2: Two-letter country codes.

- ISO 3166-1 alpha-3: Three-letter country codes.

- ISO 3166-1 numeric: Three-digit country codes.

The guidance issued by FinCEN adds another layer of complexity to AML systems because the red flags are not contained in a predefined list of country codes, but in a free text field such as a city, which creates a number of challenges.

The image below shows an address in Ciudad Juarez. Mexico and many financial institutions will have similar field definitions to capture addresses in various systems for client on-boarding or to facilitate a transaction. The only field which is based on a predefined list is the country code and sometimes the state/province, but most of the other fields are free text. However, some financial institutions will attempt to validate the address based on the information given, but not all organizations have the capacity to do so.

If most traditional AML models rely on country codes as a key attribute to determine suspicious activity, then how will a free text city be handled?

The Micro-Jurisdiction AML Model

Essentially, the FinCEN advisory is pointing to an extension of the traditional AML model where one of the additional attributes in the model would be a micro-jurisdiction. The main three components (Frequency, Amount and Jurisdictional risk) of the traditional AML model would still apply, but a fourth attribute would need to be added to the model and calibrated accordingly.

- Frequency: The number of transfers which occurred within a specific time period. Example: 3 transfers over a rolling 7 day time period.

- Amount: The value of each transfer. Example: A minimum threshold of X dollars could be configured in the monitoring system. Other elements would include round dollar amounts and amounts just below minimum reporting requirements.

- Jurisdictional risk: The risk level or score associated with each country. Example: Transfers flowing through high-risk jurisdictions would generally receive greater scrutiny than similar transactions which only flowed through low-risk jurisdictions based on the financial institution’s country risk ranking.

- Micro-Jurisdictional risk: The risk level or score associated with specific towns, zip codes or cities. Example: Transfers flowing through high-risk micro-jurisdictions would generally receive greater scrutiny than a similar transaction which only flowed through low-risk micro-jurisdictions based on the financial institution’s risk ranking.

The Implications of Micro-Jurisdictional Risk

If regulators continue to issue guidance which highlights specific geographic areas as part of a money laundering typology, then traditional AML systems must evolve or engage third party vendors which can process large volumes of data quickly, and without impacting the daily operations of the financial institution’s overall AML program. Another question which comes to mind is to what extent financial institutions should be proactive?

Should financial institutions begin to gather their own intelligence to identify potential high-risk micro-jurisdictions or should they wait for advisories from their respective regulators? The amount of intelligence gathered could be relative to the financial institution’s risk appetite and geographic footprint.

Traditional AML systems may not be the optimal solution to process large volumes of data to extract towns, zip codes and cities from free text fields. Hence, using a third party solution based on the latest advances in computing technology that can cleanse, prepare and risk rate the data before it is sent to the traditional AML systems would be beneficial to financial institutions.

Identifying and monitoring high-risk micro-jurisdictions could extend a financial institution’s AML program’s sophistication by focusing on the more granular attributes of transactional activity and consequently pushing the risk-based approach to new horizons.